In last week’s missive entitled “Beware the Secular Bear,” I covered the likelihood of the current bloodbath in American technology and meme stocks being a secular bear as opposed to a cyclical bear, where the former is years in duration rather than a few quarters. This week, I discuss the correlation between secular bear markets and gold in the context of a credit-tightening cycle, but before I begin, let it be known that the number one question I get asked constantly is “What is wrong with gold?” These queries are usually framed with the usual arguments and theses about consumer prices and currency debasement with the highly-predictable references to “stagflation” with arrows pointing, flags waving, and trumpets blaring as to the similarity with the 1970s replete with gas lines, political scandal, and angry oil-producing countries trying to cripple the West.

“Never underestimate the replacement power of equities within an inflationary spiral.” (MJB – 1980)

Unfortunately, the current fiscal and monetary landscape is anything but a 70’s-style stagflation for a number of reasons first and foremost being that the demographics are different. The Baby Boom Generation was just becoming the engine of growth for North America and once they started burning protest signs instead of brassieres and donning three-piece suits in place of bell-bottomed blue jeans, the money-printing machine that papered over the huge deficits caused by the Vietnam War and the “War on Poverty” created double-digit inflation because of the generational impact the Boomers had over money velocity. Banks loaned money to the Boomers and they spent it willingly on houses and cars and ever-increasing fuel prices during an era where the United States was the world’s largest creditor nation. Contrast that with 2022, where the exact reverse has America as the world’s largest debtor nation and as we all now know too well from our training in Econ-101, debt creation is massively inflationary while debt liquidation is the reverse.

So, with the Fed now about to embark upon a cycle of “balance sheet normalization”—otherwise known as “debt liquidation”—the world is about to resemble conditions reminiscent of the 1930’s when the Fed began draining liquidity from the system at exactly the wrong time.

This is not to suggest that we are about to enter a deflationary depression anytime soon because the Fed is run by its member banks (its owners) and the one truism upon which we can all rely is that this mountain of household debt propping up the current real estate bubble cannot be allowed to go “unsecured”—meaning—that the exact second that Jerome Powell begins to boast about the rapidly-descending CPI is the exact second that he gets called on the carpet by his Wall Street supervisors with the message that their mortgage loan books are now embroiled in terminal default with the housing collateral in virtual freefall.

Such a condition would and will result in a fork-in-the-road decision: Do we protect Main Street or do we save Wall Street? During last Wednesday’s press conference, Jerome Powell began by saying that he wanted to send a message to the American people because, and I quote, “We work for you,” at which point I wanted to take my favorite Alfred E. Neuman paperweight and hurl it at the TV monitor. To say that Powell was being disingenuous is an understatement. The Fed was never about the average citizen’s well-being; it has always been tasked with protecting the banking system which means the massive stockholdings of the elite crowd and the equity contained therein.

The week closed out with the U.S. 10-year treasury sporting a yield of 3.142%, double where it resided in January. Without the interference of the Fed and its battery of dutiful and obedient desk traders, it appears as though the bond market is experiencing the recently-rarified process known as “true price discovery” where bond vigilantes wearing peace sign necklaces and bell-bottomed blue jeans have rediscovered the practice of dumping fixed income holdings whenever governments or their “sponsored entities” misbehave either fiscally or monetarily.

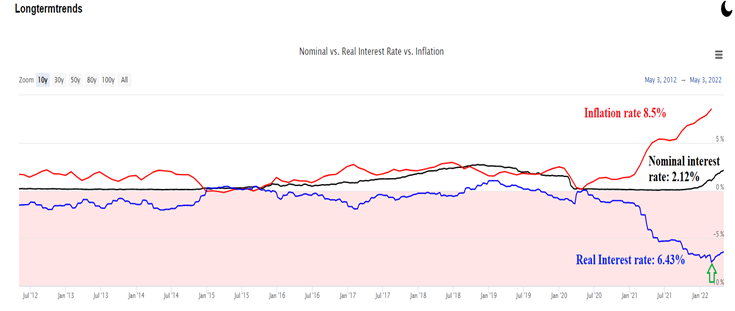

With yields rising sharply, the clarion call for the legions of gold and silver bulls—negative real interest rates—has now reversed. While the “real” cost of borrowing (defined as “the nominal interest rate minus the inflation rate”) is indeed still negative, it is no longer in the long-term downtrend that began in early 2019, long before the pandemic-induced orgy of fiscal and monetary insanity arrived. As the nominal rate of interest rises and government and central bank stimuli are removed, what is solidly in the crosshairs is CPI (inflation). If the crashing stock markets are finally allowed to be the coal mine canaries that they were before Fed interference became commonplace, then economic growth is contracting and that will undoubtedly send certain CPI components into freefall which means that the gold and silver bulls are going to be under siege because real interest rates are now struggling to go positive.

The significance of the reversal of Fed policy cannot be underestimated and no better viewing point is the chart of copper. The metal purported to have a Ph.D. In Economics has clearly read and comprehended the message conveyed by a) the FOMC and b) the global equity markets.

As my premiere choice of metals in 2022, the many reasons for owning it are all centered around the supply side of the equation. Lockdowns in China, insufficient CAPEX for the past decade, ESG constraints, and political change in Latin America have not disappeared but since price is determined by, not only supply issues, but also demand issues, the drive to vanquish the CPI enemy is also going to vanquish growth which implies reduced global demand which is exactly what the copper chart is telling us.

Alas, before investors in copper equities begin rummaging through jackets and purses for daily doses of Fentanyl and Oxycodone, it is important to revisit what I was saying a few paragraphs ago about the probable “end game” for what amounts to a veiled threat to curb price inflation. The real bear market that began in 1917 was the one that coincided with the creation of the Federal Reserve. With that event, there arrived a perpetual bear market in cash with the odd exceptions that occurred when the Wall Street gamblers tried to blow up the financial system (1930, 2008, 2020).

Jerome Powell tried to normalize the balance sheet back in 2019 and that lasted only until he was ordered to embark upon REPO in order to bail out a number of hedge funds that had gone into cardiac arrest over some bad bond bets. It was in the fall of 2021 that he pivoted from business as usual where his mandate was centered around maximum full employment citing the escalating rate of inflation as being “transitory” to a more insidious mandate that centered around price stability. However, I would ask you “What exactly has the Fed done other than jawbone the credit markets?” The 10-year yield is up over 1.50% while the Fed funds rate is up 0.5%. They are still buying copious amounts of mortgage-backed securities while doing nothing to curb the lending activities of their member back bosses.

Inevitably, the Fed is going to be forced to return to its profligate policies that, by default, condone and fortify the century-old bear market in cash. The enemy of the banks is anything one owns upon which no fee can be charged. Cash in a mattress is a non-revenue-producing asset, so banks hate it. Gold in a household safe is a non-revenue-producing asset so they hate gold too. Go down the list of underperforming assets since the Great Financial Bailout of 2008 and the two worst performers in real terms and relative to bank-controlled assets are cash and precious metals. Banks control all financial assets and they have created a bubble in housing such that homeownership is virtually impossible without the fee-based availability of a mortgage loan.

Matt Taibbi coined the greatest phrase in history when he wrote “The world’s most powerful investment bank is a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.” That phrase beautifully describes the reason that the current market malaise is the only thing that could ever be described as “transitory” because the Fed can never let anti-inflation policy moves choke off the Wall Street money machine. Unlike the 1970s, when the U.S. was the world’s largest creditor nation, choking off Wall Street has dire implications for a government running the world’s largest debtor nation.

However, since our loan officers and significant others do not reside in the “long-term” world of expectation and performance, gold, silver, and copper investors are going to be vulnerable to the deflationary sermons of central bank actors as they do their mightiest to restore their begrimed credibility by first taking down everything that can be controlled through the Crimex paper markets (which includes oil) after which they can trot it out with a yellow highlighter as proof that they “did their jobs.”

Because it involves a delicate balancing act between moderating inflation and capital market implosion, central bank jawboning is going to be a cacophony of squawks designed to convince market participants that the bear market in cash never was. At the end of the day, debt deflation, balanced budgets, and fiscal conservatism cannot be engineered within a contracting economy and deflating capital markets.

With this anti-inflation vigilance being transitory (there’s that word again), we all must strive to determine the point in time where the Fred pivots back to “accommodative.” Unless we know, as Omar Sharif said, “the moment in the evening when the cards turn for or against you,” we will have little choice but to rely on technical analysis to decipher shorter-term trends in commodities.

With this anti-inflation vigilance being transitory (there’s that word again), we all must strive to determine the point in time where the Fred pivots back to “accommodative.” Unless we know, as Omar Sharif said, “the moment in the evening when the cards turn for or against you,” we will have little choice but to rely on technical analysis to decipher shorter-term trends in commodities.

I recall a friend of mine from 2002 that was convinced that silver was going to $50/ounce so he levered up at around $4 and kept parlaying the increasing equity as prices rose such that what started as a one-contract position at $4 grew to a ten-contract position at $15 by late 2007. I watched with morbid fascination as silver underwent a massive drawdown during the 2008 subprime crisis whereby he received a USD $250,000 margin call, forcing the complete liquidation of his entire position. Of course, by 2011, silver was through USD $50/oz. thus validating the famous quote from a sophisticated brokerage client: “Do not tell me what to buy; just tell me when to buy it.”

I only relate to that story because many of my readers and subscribers own companies exploring for or developing gold, silver, copper, or uranium all of which have superb longer-term fundamentals. Importantly, margin clerks do issue cash calls based upon “longer-term fundamentals” nor do college administrators seeking tuition fees so never has the term “risk management” carried greater significance than where we are today.

As I wrote in the 2022 Forecast Issue when issuing my cautionary note regarding the impending January Barometer sell signal “Capital preservation trumps ROI for 2022."

That advice has not changed but since neither I nor anyone else can guarantee the point in the future where the Fed is called “on the carpet,” the key to surviving this shorter-term volatility lies in managing position sizes and eliminating leverage (margin). While retail sentiment is decidedly black-bearish, the true bottom of the stock market cycle arrives only when analysts halt the practice of calling bottoms in stocks that were darlings during the last bull move.

As the supreme irony concerning sector allocation, there is probably less risk in the junior resource sector dominated by companies considered “highly speculative” trading on the TSX Venture Exchange or the CSE when compared to most of the NASDAQ issuers that rely on issuing junk bonds to remain “going concerns.”

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” (Benjamin Graham)

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at miningjunkie216@outlook.com for subscription information. In my view, the levels of retail speculation since the pandemic arrived and “stimmy cheques” navigated their way into Robin Hood accounts buying trashed, over-leveraged technology or “meme” deals absolutely dwarfs the number of dollars that went to resources. As such, I believe that the junior resource names will outperform by late 2022 and possibly sooner as the in-ground replacement value of deposits results in greater appreciation in both sentiment and dollars.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to be the first to know about interesting Base Metals investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter.

Subscribe

Michael Ballanger Disclaimer

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Disclosures

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of the information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services, or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.