My history with Norseman Silver Ltd. (NOC:TSX.V) goes back to my two-decade relationship with Chairman Campbell Smyth, who operates out of Perth, Australia, and who has been a client, a colleague, a partner, and a friend. NOC rose from the ashes in 2020 with a clean capital structure, funding in place, and an intention to build assets in the silver space.

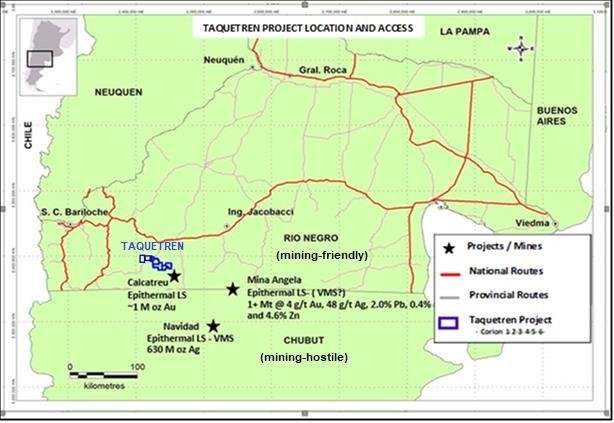

By mid-2020, however, that view expanded to include the copper narrative, as newly-appointed CEO, Sean Hurd, by way of a long-term relationship with Argentinian Daniel Bussandri, moved quickly to acquire a highly-prospective project in Rio Negro Province, located in the Gastre Fault region of Patagonian, Argentina. That project (The Taquetren Project) is the sole reason that NOC carries the second-highest weighting in my GGMA portfolio.

Norseman consulting geologist, Daniel Bussandri, has known Norseman CEO Sean Hurd since the early 2000s.

Sean was an executive with Aquiline Resources during the period in which Bussandri delivered the mighty Navidad Silver Project, which was drilled off to the tune of some five-hundred million ounces of silver after which was sold to Pan American Silver Corp. (PAAS:TSX; PAAS:NASDAQ) for over US$626 million in 2009.

It remains to this day one of the largest undeveloped silver deposits in the world. The reason it remains “undeveloped” is that in 2003, the Chubut Province legislators banned the use of cyanide in mining operations, effectively shelving the project until the laws are modified.

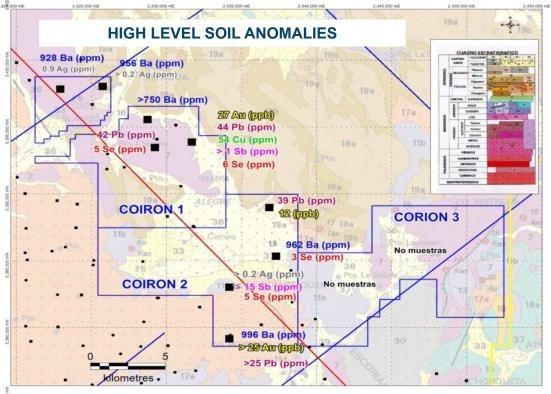

The initial results at Taquetren were quite impressive, and were this a showing in the Abitibi Greenstones or Nevada, the market would certainly have reacted last April when they reported 8% copper values in outcrops over a 300-meter-long section.

Adjacent to Chubut Province is the mining-friendly province of Rio Negro in which several operating mines are present. The Taquetren Project, located in Rio Negro, was introduced to Norseman by Daniel Bussandri in 2021, and after a brief period of due diligence, it was optioned off to NOC with Bussandri in charge of all exploration on the property.

Originally, it was my enthusiasm for silver that attracted me to the Gastre Fault region of Patagonia and primarily because of Navidad. I was familiar with Aquiline through the career of its founder, Toronto-based Mark Henderson, who I had heard speak a number of times and to whom I was introduced in the early 2000s.

Through a colleague, I followed Aquiline’s progress until the buyout by Ross Beaty’s Pan American in 2009, after which I lost track of both Argentina and Navidad. It was like a shotgun blast in 2021 when NOC’s Sean Hurd told me that he was with Aquiline during that period and that the discoverer of Navidad was a friend.

Lo and behold, several weeks later, I learned that Bussandri is the guy and Taquetren is the project and that Norseman can own 100% of the project by completing all of the work commitments contained in a beautifully back-ended deal that requires payments only after results justify further work.

The initial results at Taquetren were quite impressive, and were this a showing in the Abitibi Greenstones or Nevada, the market would certainly have reacted last April when they reported 8% copper values in outcrops over a 300-meter-long section.

The initial results at Taquetren were quite impressive, and were this a showing in the Abitibi Greenstones or Nevada, the market would certainly have reacted last April when they reported 8% copper values in outcrops over a 300-meter-long section.

There were 200 grams per tonne (200 g/t) silver values as well, but the primary focus has shifted to copper, largely because of the geology in the area and also the market’s attitude toward silver. The new generation of stock buyers seems to gravitate more toward the electric metals narrative than they do the precious metals narrative, so I view it as fortuitous that the “first pass” of sampling turned up copper grades that absolutely must be investigated further.

Bussandri knows Patagonia and has a proven “mine-finder” legacy upon which I am banking ample family capital in what I view as the ultimate leverage play on the electrification movement.

I do also acknowledge that market conditions are not exactly conducive to geochemical surveys regardless of how prospective they may be, but I have long held that companies that sit on their hands (and their treasuries) because of “challenging markets” are companies that wind up behind the curve once animal spirits return.

Now, as for the stock price, it has been a very disappointing journey during which I have participated in four placements, two ($.05 and $0.15) prior to launching this newsletter advisory and two ($0.25 and $0.33) post-launch. I attribute the weakness to the price of silver, and if you look at the chart at the top of the article, you can see the peak in Q1 2021, which was coincident with the spike in silver to US $30/oz., after which the silver market along with all of the silver producers, developers, and explorers all entered into primary bear markets with silver dropping over 43%.

There was no exclusion from the electric metals correction either, as copper fell over 38% despite looming global shortages from feeble CAPEX commitments and supply chain issues.

To NOC’s credit, Bussandri and his team have been busy conducting field sampling analysis — basic geology — to attempt to formulate a 2023 work plan that will involve geophysics and diamond drilling once they have identified targets deemed suitable for further investigation.

As we move further out from the Patagonia winter, site accessibility and working conditions will allow for an acceleration of the program such that by the time the metals market corrections have run their course, Taquetren will have sufficient field momentum to attract the attention of investors willing to speculate on a Navidad-type result — and I cannot emphasize the degree of enrichment that a world-class copper-silver discovery would create, be that in any type of market environment.

Bussandri knows Patagonia and has a proven “mine-finder” legacy upon which I am banking ample family capital in what I view as the ultimate leverage play on the electrification movement.

As for jurisdictional issues, Argentina is considered to be one of the few countries in Latin America that are not experiencing leftist political swings; it has always marched to a somewhat different drummer, but recent legislation would suggest a friendlier attitude toward foreign investment with particular attention to mining.

More recently, legislation in Chubut Province has paved the way for partial development of the Navidad deposit, subject to environmental approvals, which would constitute a huge stride toward opening up this underexplored region to job-friendly exploration and development.

Norseman Silver Inc. intends to soon commence with an aggressive marketing program with its primary focus on Taquetren and its unique position as a “first mover” in the region, but with neighboring companies such as Patagonia Gold having already established mining operations (Calcatreu), this provides necessary infrastructure (roads, power, etc.) also accessible to NOC.

Ergo, Norseman Silver Inc. at its current depressed market cap represents a similar risk-reward allocation for risk-oriented individuals. I will not assign a target price just yet, but it certainly has all the pieces to command a pre-discovery market cap of somewhere north of $20 million or CA$0.30 per share between now and year-end.

I elected to assign a significant weighting to Norseman Silver in 2020 based on my assessment of the management group. Chairman Campbell Smyth is well-schooled in the resource sector and is not only a highly successful investor in this space, but he also understands the prerequisites for success at the Board level. Sean Hurd has experience navigating the Argentinian regulatory landscape and has enjoyed great success in the past from his tenure with Aquiline.

However, the one individual that will drive valuation is none other than Argentinian Daniel Bussandri, whose extensive years roaming the Patagonian countryside have provided him with intimate knowledge of and free-reign access to some of the most highly-prospective, unexplored prospects in the region.

I see junior resource markets experiencing a rebirth in the fourth quarter of 2022, brought on by a softening of the harsh rhetoric being doled out by the U.S. Fed and a downside reversal in the

U.S. dollar. Once concern shifts from inflation to resource shortages, the electrification movement will be once again front-and-center, so companies like Norseman Silver will be hitting the pavement in full stride with full intent to repeat the success enjoyed by Aquiline shareholders thirteen years ago. The US$626 million paid for Aquiline (its only real value was Navidad) was approximately CA$663 million, with silver north of US$17/ounce. With Norseman’s capital structure at 67.7 million (fully diluted) (See below), a Navidad-type buyout would be CA$9.80 per share, and while there is a great deal of drilling and development work to be done (successfully) prior to an event such as that, and given the players in this game, it appears as though NOC’s current CA$7.44 million market cap does not reflect anything close to the upside leverage contained in Taquetren.

I expect that more results will be out shortly that will hopefully augment the excitement that was palpable last April when the exploration team led by Bussandri reported the copper values at the Veta Juan zone. The mineralization seems to emerge and submerge along a 5-kilometer stretch of ground on what is believed to be a volcanic caldera complex, so the potential for world-class scale is definitely there.

In sum, you have all read other newsletter “gurus” (tongue firmly implanted in cheek) revisit one of their “clangers” that are usually down 80-90%, usually after a 2008-style or 2020-style stock implosion where the speculative stocks get pitched overboard on the assumption that they will never recover.

A case in point was Aftermath Silver Ltd. (AAG:TSX.V), (one of my picks from the 2020 Forecast Issue) which fell from a January 2020 high of CA$0.54 to a paltry CA$.09 during the COVID Crash only to regain its footing later in the year and go out at a high of CA$1.70 in early January of 2021. I recall emails from former shareholders questioning my sanity that I was still buying AAG in March 2020 in light of the fact that the world was surely “coming to an end.”

It surely did not end, and I was actually proven “sane.” You can go right down the list of junior companies mauled in those market corrections, and those in the list of the GGM Advisory all came roaring back largely because while they are speculative in nature, they have solid management and above-average projects.

Ergo, Norseman Silver Inc., at its current depressed market cap, represents a similar risk-reward allocation for risk-oriented individuals. I will not assign a target price just yet, but it certainly has all the pieces to command a pre-discovery market cap of somewhere north of $20 million or CA$0.30 per share between now and year-end.

Buy Norseman Silver up to CA$0.20 (subject to revision on news).

Want to be the first to know about interesting Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter.

Subscribe

Michael Ballanger Disclaimer

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Disclosures:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Norseman Silver Inc. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: Norseman Silver Inc.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Norseman Silver Inc. and Aftermath Silver Ltd., companies mentioned in this article.

Charts are provided by the author.